Credit Card Personalization Architecture: The ML Stack That Actually Works

Most banks have the data to personalize credit card offers at scale. Most can't actually do it in production because their ML architecture wasn't designed for real-time decisioning. Here's what the right stack looks like — and why the wrong one loses to Amazon.

Table of Contents

Here is the uncomfortable truth about credit card personalization at banks: the data advantage is real, and the technical execution is poor enough that it doesn’t matter.

A major U.S. bank has 10–40 million cardholders. It has years of transaction history, spend category data, payment behaviour, credit utilisation patterns, balance transfer history, channel interaction logs, life events (new mortgage, salary change, first child), and in many cases biometric and behavioural authentication data. Amazon, for all its recommendation sophistication, has purchase history and browse data. It doesn’t know your FICO score or whether you carry a revolving balance.

Banks lose on personalization because their ML architecture is a decade behind their data, and the gap compounds. This post describes what the right architecture looks like and, more usefully, why the wrong architecture is so common — because understanding the failure modes is how you avoid building another one.

The Core Problem: Batch-First Architecture in a Real-Time World

The standard bank ML architecture for card offers was designed in an era when “real-time” meant “daily batch.” A nightly job runs propensity models over the customer base, scores every customer against every product, applies eligibility rules, ranks the output, writes results to a campaign management database, and the next morning’s digital banking session shows the winning offer.

This pipeline has a structural latency of 12–36 hours. The customer event that most predicts card application intent — a large purchase on an existing card, a credit utilisation spike, a salary deposit that’s 30% above normal, a competitor card application pulled in the bureau — happens now, and the personalization system doesn’t respond to it until tomorrow.

Amazon doesn’t have this constraint because Amazon’s architecture was built around the browse session as the fundamental unit of personalisation. The bank’s architecture was built around the nightly campaign file as the fundamental unit of marketing.

Rebuilding a bank’s personalisation architecture is a $20–50M program. Most banks choose to optimise the batch pipeline instead. This is correct short-term and wrong at the architecture level, and the decision accumulates technical debt that makes the eventual rebuild harder.

The Four Architectural Layers

A production-grade credit card personalisation system has four distinct layers, each with different latency requirements, data access patterns, and failure modes.

Layer 1: Signals

The signals layer is the data ingestion and stream processing infrastructure that produces the raw inputs to the personalisation system. It operates at three latency tiers.

Real-time signals (< 1 second):

- Current digital banking session: pages viewed, cards browsed, time-on-page

- Current transaction context: amount, merchant category, channel

- Authentication risk score from the identity system

- Current account balances and credit utilisation

Near-real-time signals (1 second – 15 minutes):

- Recent transaction events (Kafka consumer with micro-batch aggregation)

- Call centre interaction flags

- Alert acknowledgements and notification responses

- A/B test assignment and variant state

Batch signals (1 hour – 7 days):

- Transaction aggregates (30-day spend by category, 90-day payment history)

- Credit bureau refresh (monthly, with intra-cycle triggers for material changes)

- Propensity model scores (pre-computed for all customers)

- Segment and lifecycle stage assignments

- Competitor intelligence flags (balance transfer inquiry patterns)

The signals layer’s primary design challenge is not the individual signal — it’s the join. Combining a real-time session signal with a 30-day spend aggregate and a monthly bureau refresh requires careful management of which signals are available at what latency, and what to serve when a signal is stale or missing.

Layer 2: Feature Store

The feature store is the most under-engineered component in bank personalisation stacks and the most common reason projects fail.

What the feature store needs to do:

- Serve features at low latency (< 10ms) for real-time decisioning

- Maintain consistency between online serving and offline training (training-serving skew is the leading cause of production model degradation)

- Support point-in-time correct feature retrieval for offline training (to prevent data leakage)

- Version features and model bindings together

- Serve precomputed features for the 95% of customers who aren’t in an active session

The feature hierarchy for card personalisation:

Customer-level features (precomputed, refreshed in batch):

- credit_score_band (FICO range, refreshed monthly)

- revolving_utilisation_90d (average over 90 days)

- payment_consistency_score (on-time payment rate, last 12 months)

- spend_category_vector (spend % by MCC category, last 90 days)

- product_affinity_scores (precomputed propensity per card product)

- lifecycle_stage (new, developing, mature, at-risk, churning)

- income_band (estimated, from transaction patterns)

- household_size_signal (number of linked accounts, shared address)

Account-level features (refreshed hourly or on event trigger):

- current_utilisation (real-time balance / limit)

- days_since_last_payment

- recent_large_purchase_flag (transaction > $2000 in last 7 days)

- competitor_inquiry_flag (bureau pull from competitor in last 30 days)

Session-level features (real-time, available only during active session):

- session_entry_point (direct, search, notification, email)

- cards_viewed_this_session (list of product pages visited)

- time_spent_on_cards_page_seconds

- device_type (mobile, desktop, app)

- session_risk_score (from authentication system)Critical design principle: feature groups, not feature columns. A feature store that exposes individual feature columns forces every model to specify 40+ features by name. A feature store that exposes logical groups (credit_risk_features, spend_behaviour_features, session_context_features) lets models evolve independently.

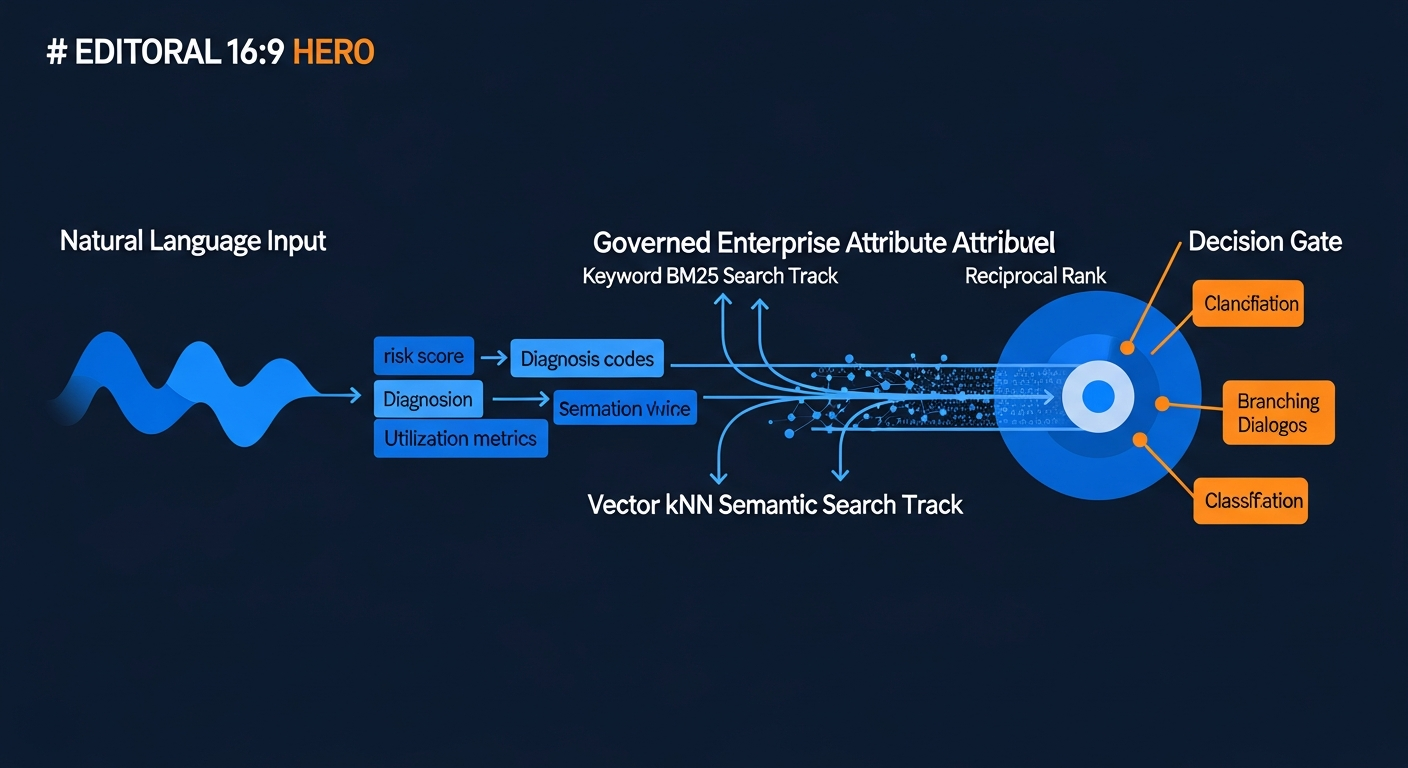

Layer 3: Decisioning

The decisioning layer is where the personalisation happens. The right architecture is a cascade, not a single model.

Stage 1: Eligibility filter (hard rules, < 1ms)

Before any ML runs, filter the candidate offer set to legally eligible products. This is not optional and not an ML problem.

def eligibility_filter(customer_id: str, offer_catalog: list) -> list:

"""

Hard constraints that cannot be overridden by ML scores.

These encode regulatory requirements, credit policy, and product terms.

"""

customer = feature_store.get(customer_id, groups=["credit_risk"])

eligible = []

for offer in offer_catalog:

# ECOA: cannot discriminate on protected classes — enforced via

# credit policy criteria that don't use protected attributes

if offer.min_credit_score and customer.credit_score < offer.min_credit_score:

continue

if offer.max_dti and customer.debt_to_income > offer.max_dti:

continue

# State-specific: some products not available in all states

if customer.state not in offer.eligible_states:

continue

# Portfolio concentration: don't offer if customer already holds this product

if offer.product_id in customer.existing_products:

continue

eligible.append(offer)

return eligibleStage 2: Propensity scoring (gradient boosted trees, < 10ms)

Score each eligible offer for this customer’s likelihood to apply and activate. GBT (XGBoost or LightGBM) is the right model class here for three reasons: it handles tabular features well, it’s interpretable enough for regulatory review, and it’s fast enough for online serving.

# Feature vector for propensity model

features = feature_store.get(customer_id, groups=[

"credit_risk_features",

"spend_behaviour_features",

"product_affinity_features",

])

# One score per eligible offer

propensity_scores = {}

for offer in eligible_offers:

X = build_feature_vector(features, offer)

propensity_scores[offer.id] = propensity_model.predict_proba(X)[1]Stage 3: Contextual ranking (Thompson Sampling or LinUCB, < 5ms)

The propensity model is trained on historical data. The contextual bandit is optimised on live feedback. Use the bandit to rerank the propensity-scored offers, weighting exploration vs. exploitation based on how much data you have for this customer-offer pair.

context = feature_store.get(customer_id, groups=["session_context_features"])

context_vector = build_context_vector(context, session_data)

# Rerank using Thompson Sampling

final_ranking = []

for offer_id, propensity in sorted(propensity_scores.items(),

key=lambda x: -x[1]):

ts_score = bandit.thompson_sample(arm=offer_id, context=context_vector)

combined = 0.6 * propensity + 0.4 * ts_score # blend: exploit history + explore live

final_ranking.append((offer_id, combined))

final_ranking.sort(key=lambda x: -x[1])

top_3 = [offer_id for offer_id, _ in final_ranking[:3]]Stage 4: LLM reranking and copy personalisation (optional, 50–200ms)

For high-value customer segments, pass the top-3 offers and customer context to an LLM to generate personalised offer framing. This is the newest layer and the most expensive — reserve it for customers where the incremental revenue justifies the latency and cost.

if customer.segment in ["premium", "high_value"]:

personalized_copy = llm_client.generate(

prompt=build_personalisation_prompt(customer_context, top_3_offers),

max_tokens=150,

temperature=0.3,

)Layer 4: Delivery

The delivery layer handles channel selection, frequency capping, timing optimisation, and A/B test assignment. It’s often the most complex layer operationally because it has to coordinate across digital, mobile, branch, call centre, and direct mail — each with different latency requirements and content constraints.

The most common failure in the delivery layer is channel inconsistency: the customer sees Offer A in the mobile app and Offer B in the email they receive 30 minutes later, because the two channels draw from different decisioning paths with different refresh rates.

The correct solution is a decisioning service that all channels call, with channel-appropriate presentation logic applied at the delivery layer rather than at the decisioning layer. One decision per customer per session, surfaced across all channels.

Why Most Bank Personalization Projects Fail

Failure mode 1: Feature store built as a data warehouse view.

The most common mistake. A Redshift or Snowflake view is fast enough for batch models but 100–1000× too slow for real-time serving. Teams build real-time serving on top of batch infrastructure and either accept high latency or build a separate serving layer that immediately creates training-serving skew.

Failure mode 2: One big model instead of a cascade.

Teams build a single neural network that takes all features and produces a ranked offer list. It outperforms the baseline in A/B tests. It fails in production because: it’s slow (200–500ms per customer), it requires expensive retraining when offer catalogs change, it’s a black box for regulatory review, and it can’t separate eligibility enforcement from propensity scoring.

Failure mode 3: ML ownership in the wrong team.

Card personalization ML requires deep collaboration between credit risk (who owns the eligibility logic and regulatory exposure), marketing (who owns the offer catalog and campaign calendar), engineering (who owns the serving infrastructure), and data science (who owns the models). When ML ownership sits entirely in marketing analytics, the result is batch models optimised for campaign metrics. When it sits in engineering, the result is technically excellent infrastructure with no business context. Neither works.

Failure mode 4: Not instrumenting the bandit.

Teams deploy a contextual bandit and don’t instrument it properly. The bandit learns and adapts, but nobody can explain why it’s showing certain offers to certain customers. Regulators ask. The answer is “the model decided.” That’s a finding.

Architecture Impact

The right credit card personalisation stack changes several things about how banks operate:

Speed to market for new products. With a feature store and model cascade in place, launching a new card product into the personalisation engine is a configuration change (add to the offer catalog, define eligibility rules, initialise bandit arms) rather than a model training project. This reduces time-to-personalisation from months to weeks.

Test-and-learn velocity. A contextual bandit with proper instrumentation can run hundreds of simultaneous “experiments” — each offer-customer-context combination is effectively its own experiment — without the overhead of formal A/B test setup. Marketing teams can iterate on offer framing weekly rather than monthly.

Regulatory defensibility. A well-documented cascade architecture is significantly easier to explain to regulators than a black-box neural network. “Here is the eligibility filter, here is the propensity model with these features and this validation, here is the bandit with these arms and this update rule” maps cleanly onto SR 11-7’s model governance requirements.

Cost structure. Real-time ML serving at scale (10M+ customers, 100M+ daily sessions) is expensive. The cascade architecture concentrates compute cost at the stages where it adds the most value (propensity scoring for top candidates, LLM personalisation for high-value segments) rather than running expensive models for every customer in every session.

Production Benchmarks

Based on published results from banks and fintechs that have implemented production-grade card personalisation systems:

| Metric | Batch baseline | Real-time cascade |

|---|---|---|

| Offer click-through rate | 2–4% | 6–11% |

| Application conversion | 1.5–3% | 3.5–6% |

| Time to personalise new product | 8–12 weeks | 1–2 weeks |

| Feature latency (p99) | 12–36 hours | 8–50ms |

| Decisioning latency (p99) | N/A (batch) | 45–120ms |

| A/B test cycle time | 30–60 days | Continuous (bandit) |

| Model-to-production time | 6–12 weeks | 2–4 weeks |

The conversion rate improvement (3–6% vs. 1.5–3%) compounds. At 10M monthly eligible sessions and an average card activation value of $200 in net interchange revenue over 12 months, the difference between 2% and 5% conversion is $60M per year. The infrastructure to deliver it costs $5–15M to build and $2–5M per year to operate.

The SuperML Take

Credit card personalisation is the highest-ROI application of ML in retail banking, and it’s chronically underinvested relative to its potential. The reason isn’t lack of data or lack of model sophistication. It’s an architectural mismatch between what the data science team can build and what the infrastructure team has deployed.

The cascade architecture described here isn’t novel — it’s what every mature personalisation organisation has converged on. The innovation is in the specific banking context: the eligibility layer that encodes credit policy and regulatory constraints, the feature hierarchy that navigates a bank’s complex data landscape, and the bandit layer that enables continuous learning without formal experiment cycles.

Banks that get this right in the next 24 months will own a structural advantage in retail card acquisition. The offer that arrives at exactly the right moment, framed for exactly this customer’s situation, with copy that reflects their spend behaviour — that wins against a generic offer with a higher APR and a national advertising campaign. Banks that don’t build the infrastructure won’t be able to compete on personalisation regardless of how good their models are, because the models will always be working from yesterday’s data.

Sources

- Feature Stores for Machine Learning — Feast Documentation

- Real-Time Machine Learning: Challenges and Solutions — Chip Huyen (2022)

- Contextual Bandits for Real-World Applications — Microsoft Research

- ECOA and Fair Lending in Model Risk — OCC Bulletin 2021-23

- LightGBM: A Highly Efficient Gradient Boosting Decision Tree — NIPS 2017

Enterprise AI Architecture

Want more enterprise AI architecture breakdowns?

Subscribe to SuperML.