Explaining Frauds in Finance: A Real-World ML Example with Credit Card Authorization

A deep dive into real-time fraud detection with Credit Card Authorization using XGBoost, SHAP, and more

· SuperML.dev · agenticAI ·

In the world of digital finance, fraud detection has evolved from simple rule-based filters to real-time AI-powered defenses. This post dives into how we can build and explain a machine learning model to detect fraud in credit card authorization, using real Kaggle data, XGBoost, and SHAP.

🔍 Why Fraud Detection Matters

Fraudulent transactions in real-time systems (like credit card payments) can cause serious financial damage if not blocked instantly. The challenge: catching sophisticated patterns in milliseconds, without blocking good customers.

📊 Credit Card Fraud Detection Dataset

The dataset used in this post is a real-world anonymized dataset made available by researchers from ULB (Université Libre de Bruxelles) and hosted on Kaggle. It is commonly used for benchmarking fraud detection models.

🧾 Dataset Overview

- Total Records: 284,807 credit card transactions

- Fraud Cases: 492 (≈0.172% of total)

- Classes: Binary classification

0= Legitimate transaction1= Fraudulent transaction

🧠 Feature Description

Time: Seconds elapsed between first transaction and this one (used for behavior tracking)Amount: Transaction amount (used for scaling and detecting anomalies)V1toV28: Principal Components derived from a PCA transformation of original features (keeps privacy intact)Class: Target label (fraud or not)

Note: The original merchant, cardholder, location, and POS data have been anonymized, so advanced behavioral feature engineering is limited unless re-constructed via surrogate features (e.g., frequency, velocity, etc.)

📥 Download Method

We used the kagglehub library to programmatically download the latest version:

import kagglehub

import pandas as pd

path = kagglehub.dataset_download("mlg-ulb/creditcardfraud")

df = pd.read_csv(path + "/creditcard.csv")This makes the pipeline reproducible and portable for Colab, SageMaker, or local notebooks.

🧪 Feature Engineering Techniques & Importance

Feature engineering is a key part of building high-performing fraud detection systems, especially when working with anonymized or abstracted features like PCA components (V1 to V28). Here’s what we focused on:

🎯 Key Techniques Used

# Time since last transaction for a given PAN (if available)

df['txn_timestamp'] = pd.to_datetime(df['Time'], unit='s')

df = df.sort_values(['PAN', 'txn_timestamp'])

df['time_diff'] = df.groupby('PAN')['txn_timestamp'].diff().dt.total_seconds().fillna(0)

# Transaction amount relative to average (per PAN)

df['avg_txn_amount'] = df.groupby('PAN')['Amount'].transform('mean')

df['amount_ratio'] = df['Amount'] / (df['avg_txn_amount'] + 1e-6)

# Velocity feature: transactions per hour (rolling)

df['txn_count_hour'] = df.groupby('PAN')['txn_timestamp'].rolling('1H').count().reset_index(level=0, drop=True)

# First-time merchant flag (if Merchant ID available)

df['is_new_merchant'] = ~df.duplicated(subset=['PAN', 'Merchant_ID'])

# POS manual entry risk flag

df['is_manual_entry'] = (df['POS_Entry_Mode'] == 'manual').astype(int)🧠 Importance

These features help the model learn fraud-specific patterns, such as:

- Rapid fire transactions (velocity attack)

- Large, abnormal amounts

- Geo-anomalies (distance jumps)

- Risky entry modes (manual entries)

⚙️ Model Training and Evaluation

🔧 Hyperparameter Tuning with Optuna

To further improve model performance, we can use Optuna — a powerful hyperparameter optimization framework that integrates easily with XGBoost.

import optuna

import xgboost as xgb

from sklearn.model_selection import cross_val_score

from sklearn.metrics import roc_auc_score

# Objective function for tuning

def objective(trial):

params = {

'objective': 'binary:logistic',

'eval_metric': 'auc',

'scale_pos_weight': scale_weight,

'max_depth': trial.suggest_int('max_depth', 3, 10),

'eta': trial.suggest_float('eta', 0.01, 0.3),

'gamma': trial.suggest_float('gamma', 0, 5),

'subsample': trial.suggest_float('subsample', 0.5, 1.0),

'colsample_bytree': trial.suggest_float('colsample_bytree', 0.5, 1.0)

}

model = xgb.XGBClassifier(**params, use_label_encoder=False)

scores = cross_val_score(model, X_train, y_train, scoring='roc_auc', cv=3)

return scores.mean()

# Run study

study = optuna.create_study(direction='maximize')

study.optimize(objective, n_trials=30)

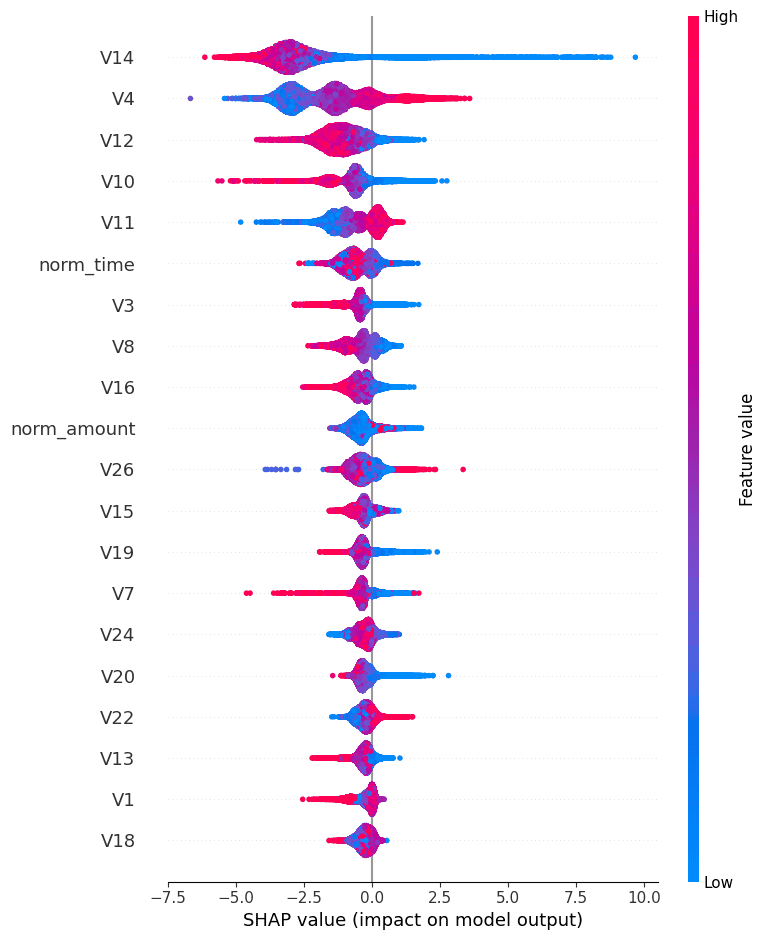

print("Best hyperparameters:", study.best_params)🧠 SHAP Summary Plot

🔬 Single Transaction Explanation

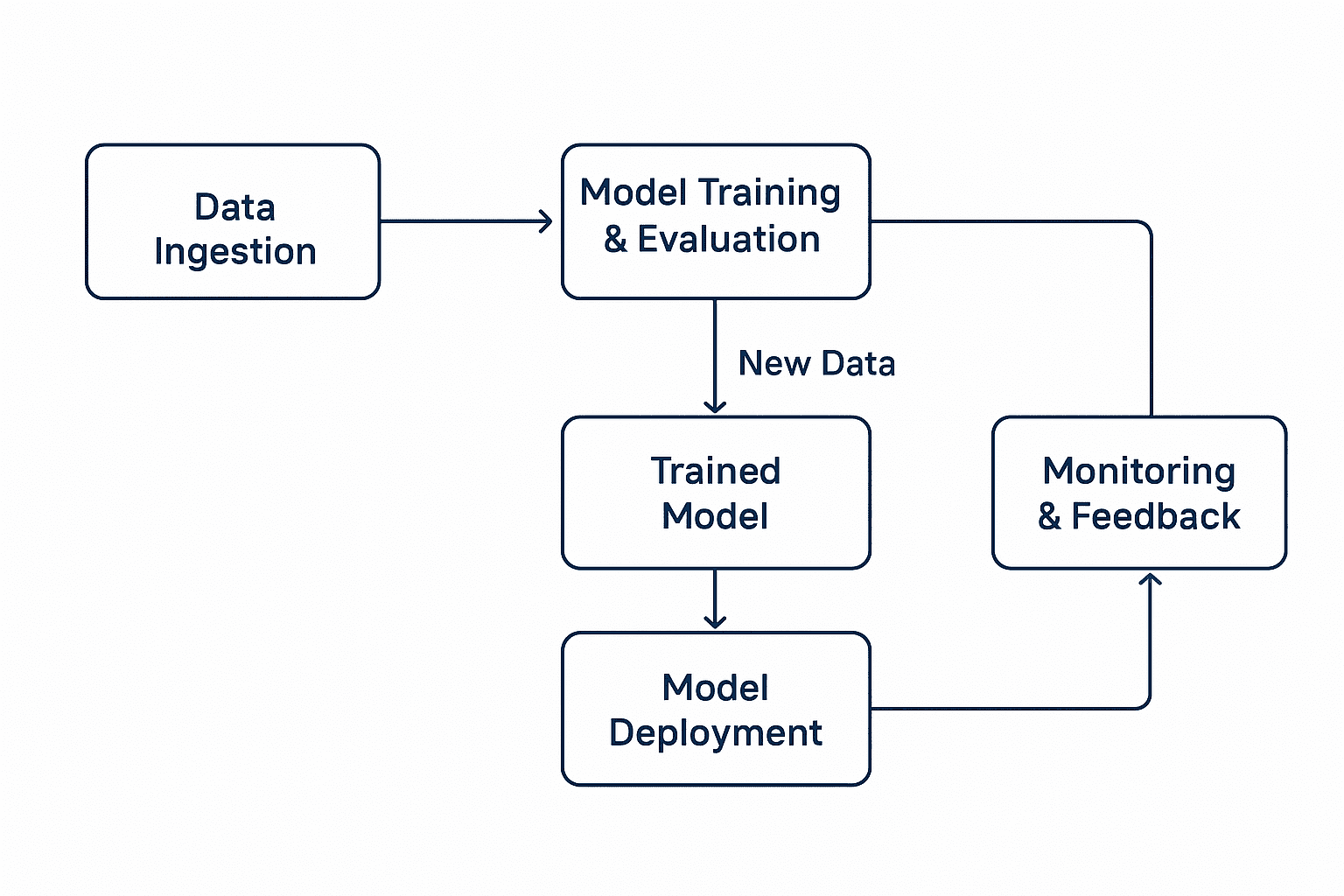

🧰 MLOps Architecture

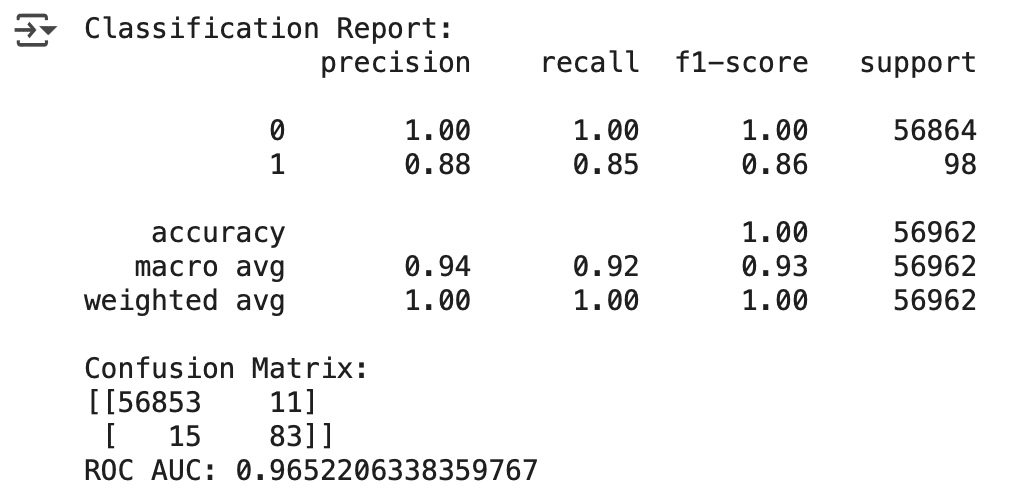

Model Performance

Fraud Detection Model Performance:

There is always space for improvement, Give your idea and suggestions on mode improvement Fraud Detection Model Performance

Give me your thoughts about these performance matrix.

Colab Notebook:

https://colab.research.google.com/drive/1tEo_JU8ao37mSKZdt3UjSC7CRM9WnzL7?usp=sharing

🔮 Coming Soon: Agentic AI for Financial Fraud Detection

In our next blog post, we’ll go beyond static models and build a full Agentic AI system that can:

- Orchestrate fraud detection using LangChain agents

- Query historical transaction data

- Explain and summarize suspicious behavior

- Trigger retraining or alerts using reasoning-driven logic

👉 Stay tuned as we turn this fraud detection model into an intelligent fraud-detecting agent.

{kind=link}